Eligibility & Payment

Executive Condominium

Eligibility Criteria

To qualify for an Executive Condominium, buyers must meet specific criteria, such as being a Singaporean citizen, forming a family nucleus, and having a household income under S$16,000. There are also requirements for a minimum stay of 5 years before selling.

You have to qualify for any of the eligibility schemes:

· Public Scheme

· Fiancé/Fiancée Scheme

· Orphans Scheme

· Joint Singles Scheme

· You must be a Singapore Citizen (SC)

. At least 1 other applicant must be a SC or Singapore Permanent

Resident (SPR)

. All singles must be SCs if they apply under the Joint Singles Scheme

· At least 21 years old

. At least 35 years old, if they apply under the Joint Singles Scheme

A subsidised housing unit refers to:

· A flat bought from HDB

· A resale flat bought with CPF housing grant

· A Design Build and Sell Scheme (DBSS) flat bought from a property

developer

· An EC unit bought from a property developer

. Other forms of housing subsidy (e.g. enjoyed benefits under the

Selective En bloc Redevelopment Scheme (SERS), privatisation of

HUDC estate, etc)

If you have not taken a housing subsidy before, you are a first timer and

may buy an EC unit from a property developer.

If you have taken a housing subsidy, you are a second-timer and may buy

an EC unit from a property developer. You have to pay a resale levy. Find

out more on the resale levy payable.

If you have already bought 2 subsidised housing, you will not be eligible to

apply or be listed as an essential occupier to buy an EC unit from a

property developer.

If you or any persons listed in the application have an interest in any HDB

flat, you must dispose of the interest within 6 months of completion of

the EC purchase.

Your monthly household income must not exceed $16,000.

All applicants and occupiers listed in the flat application:

· Must not own or have an interest in any local or overseas private

property

. Have not disposed of any private property in the last 30 months

before the application to buy an EC unit from a property developer

Private properties include but are not limited to houses, buildings, land, EC

units and privatised HUDC flats. You are deemed as having acquired

interest in a property which is:

· Acquired by gift

. Inherited as a beneficiary under a will or from the Interstate

Succession Act

· Owned, acquired, or disposed of through nominees

Prior consent must be obtained from the Official Assignee (OA) or the

private trustee for the purchase of an EC unit.

However, occupiers who are bankrupts do not need prior consent.

Cancellation of application after booking a flat

If you booked a flat and subsequently cancel your booking, you must wait

out a 1-year period from the date of the cancellation before you may

apply or be listed as an essential occupier to buy an EC unit from a

property developer.

Terminated the Sale and Purchase Agreement for an EC/ DBSS flat

If you had previously bought an EC unit/ DBSS flat from a property

developer and subsequently terminated the Sale and Purchase

Agreement, you must wait out a 5-year period from the date of the

termination before you may apply or be listed as an essential occupier to

buy an EC unit from a property developer.

Standard payment schemes for

Executive Condominium

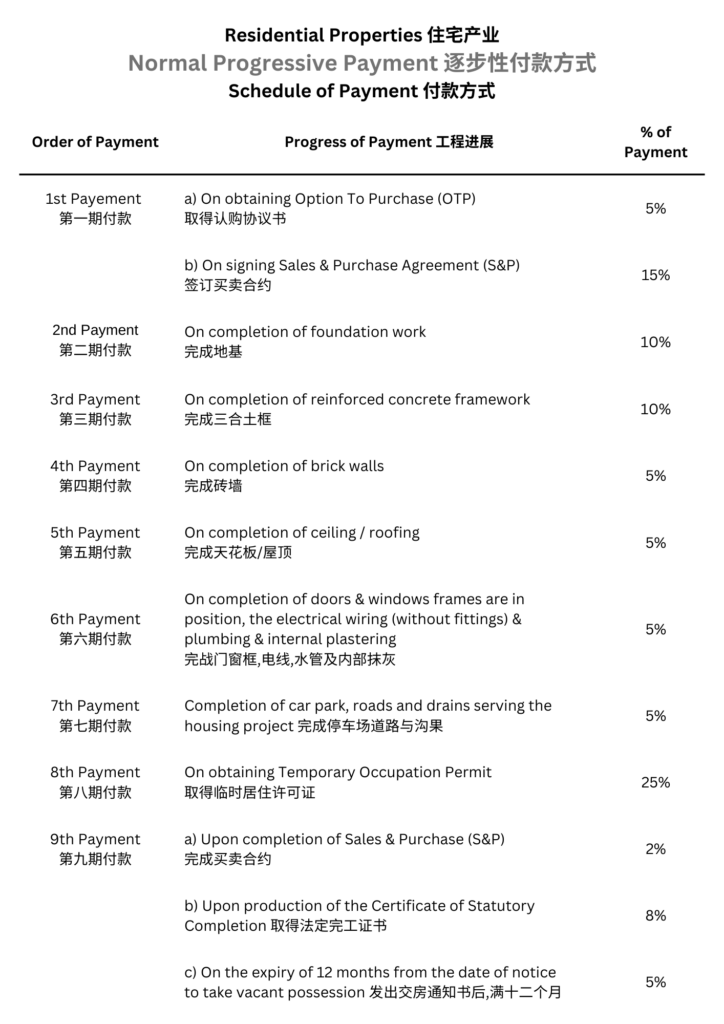

NPS

Normal Progress Payment Scheme

NPS is how a buyer would normally pay, based on the property’s completion process.

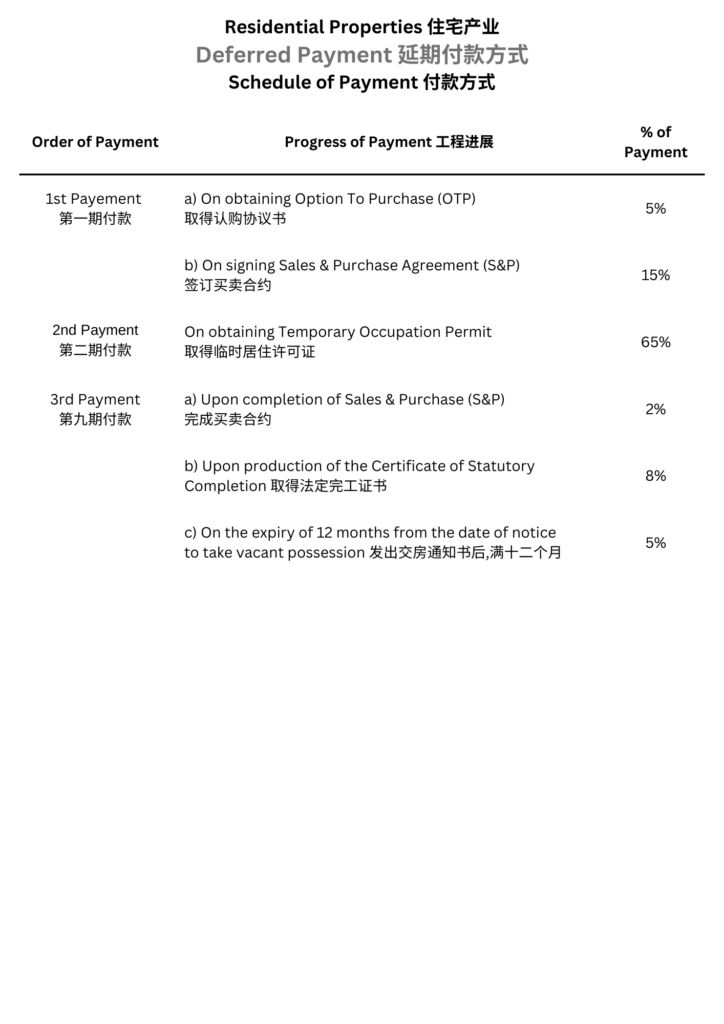

DPS

Deferred Payment Scheme

Only pay 20% + 5% downpayment. The remaining 75% can be paid once the project receives its TOP.

Standard payment schemes for

Executive Condominium

NPS

Normal Progress Payment Scheme

NPS is how a buyer would normally pay, based on the property’s completion process.

DPS

Defer Payment Scheme

Only pay 20% + 5% downpayment. The remaining 75% can be paid once the project receives its TOP.

Which payment scheme suit you?

NPS

Normal Progress Payment Scheme

Payment in Stages

Payments are made progressively in stages, aligned with the construction progress, allowing buyers to service their loan through monthly installments.

Loan Repayment

Buyers need to begin repaying their mortgage loan immediately, as payments are due according to the construction schedule.

Lower Purchase Price

The purchase price under the NPS is generally lower than the Deferred Payment Scheme, making it more affordable upfront.

DPS

Defer Payment Scheme

No Loan Repayment During Construction

Buyers do not need to service their mortgage loan during the construction period, offering flexibility for those with existing loan commitments.

Deferred Payment

Only a 20% downpayment is required initially, with the remaining 65% deferred until the property receives the Temporary Occupation Permit.

Higher Purchase Price

The purchase price under DPS is typically 2-3% higher than the NPS, reflecting the deferred payment benefit.